![]()

“You should make a budget.” The B-word itself is enough to make most of us squirm in our chairs. After two decades of helping individuals and families get a grasp on their spending, I’ve concluded that traditional “budgeting” simply doesn’t work for most people.

That’s not to say it can’t work for some. If you have enough data and you’re organized enough to know how much you’ve been spending on certain categories in the recent past, creating a budget helps many to think first before blindly spending money they may or may not actually have.

Here’s the problem: Most of us have so many methods of spending money (credit cards, debit cards, cash, Venmo, crypto, etc.) that tracking proves difficult. There are too many transactions, too many categories, and too many different accounts to keep track of.

Financial aggregators can help, but even websites like Mint.com require monthly maintenance and double-checking to make sure the algorithm has properly categorized your gas purchase at Mobil as fuel and not as a cellphone bill. It’s still not completely automated.

The primary purpose of budgeting is to remain aware of how much money is coming in and out so you can change spending behavior before cash flow crosses into negative territory.

Most budgets focus on spending by category and set limits for each. I’ve found two main flaws in this approach:

First, it violates the “KISS” principle, which suggests systems should be as simple as possible. Budgeting by category makes the process more complicated than it needs to be. Secondly, if I’ve budgeted $300 for entertainment each month and find that I’ve only spent $150 on Day 29 of the month, I may be tempted to find a way to spend it. After all, that’s what was budgeted for!

At the end of each month, categories don’t really matter. It can be nice to know, for example, what I spend on fuel each month. Then if I get the opportunity to work from home, I know what the change is worth to me. But even without budgeting by category, that can always be looked at in isolation if necessary.

Cash Flow Forecasting as an Alternative to Budgeting (Best for Those Who Pay Off Credit Cards in Full Each Month)

The most important element of any financial plan is the cash flow forecast. I’ve worked with hundreds of households over the years. I can assure you that a household that knows what expenses are coming and how they compare to projected income has a pretty good idea of what the future will bring. Those who only have a fuzzy idea of their expenses and income have a tough time planning and forecasting. That often leads to stress and anxiety.

Think of cash flow forecasting as a diagnostic device. Instead of figuring out how much you can spend, you need to know how much you’ve spent. Looking back six to 12 months in each account from which you spend (typically bank withdrawals or transactions and credit card payments) is the most accurate way to estimate your spending.

If you find you’ve averaged $6,000 per month on your credit card (or cards) and around $4,000 per month on your bank withdrawals, then you know that you’ve been spending around $10,000 per month.

Assuming you are an employee with taxes withheld from your paycheck, you can take taxes out of the equation for the time being. If you’re self-employed, you can simply create a separate quarterly expense for estimated tax payments.

Once you have a good idea of what you’ve been spending, you can start to combine monthly (or even weekly or biweekly) cash flow projections. Simply build yourself a spreadsheet in Microsoft Excel or Google Sheets. Put your monthly net income at the left, then record the expenses from your bank and credit cards (which ultimately get paid from your bank as well), and calculate your resulting balance at the far right. (Be sure not to double-count your credit card payment in both your bank and credit card expenses.)

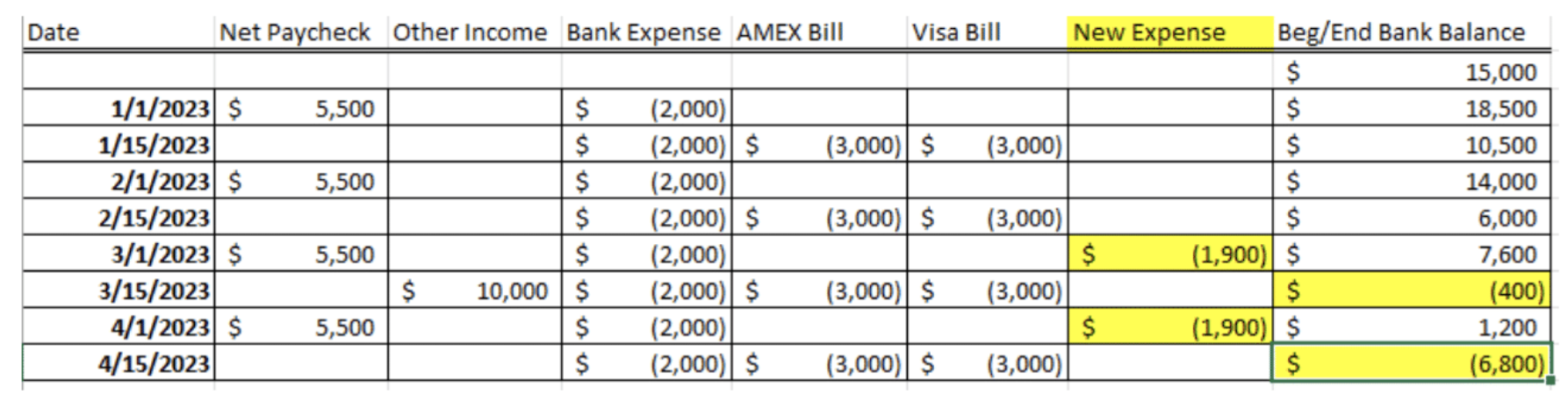

An example might read as follows:

You can add as many rows as you like to be as granular as you’d like. You might just need to see one row per month, or you might want one row for each week or pay period. To more accurately see how my bank balance will react in the coming months, I like to split my monthly bank expenses in half and spread them so half the expenses are shown on each row every two weeks.

You might expect to receive a minimum bonus at work each March. You can build that in (as a best or worst case) and see how your bank balance is affected. Maybe you’re considering a new home and want to see how that additional mortgage payment would impact cash flow. You might be receiving a gift or inheritance and want to see how that impacts the numbers. Without consulting high-end software, you can quickly see trouble brewing down the road before it surprises you

Above, it becomes clear that a problem looms. By March, credit card balances may not be something we can pay off in full without running into an overdraft situation.

Seeing this problem in advance allows us to adapt and prepare. We can set goals, such as spending no more than $4,000 each month on credit cards instead of the usual $6,000. If it becomes clear that this isn’t possible, we know that buying that new home will need to wait.

Most bad cash flow situations arise because negative cash flow sneaks up on us. By simply making a spreadsheet where the column on the far right equals the sum of the previous row’s dollar amounts and your bank account balances, you’ll see these problems well in advance and make the necessary adjustments. You can project weeks, months, or even years!

Knowledge is Power

In contrast to budgeting a certain amount for groceries and a certain amount for gas, you’ll begin to look at your credit card as your change lever.

For most of us, our bank expenses are fairly fixed. Our utilities, rent, and similar expenses are withdrawn from here each month. ATM withdrawals, one-off checks, and PayPal transactions may be withdrawn from here as well, but in general, monthly expenses are more predictable in the bank than with credit cards that get used for travel, dining, entertainment, and clothing purchases.

Instead of worrying about categories, you’ll find yourself looking at your credit card balance halfway through your billing cycle and asking yourself, “How much am I on pace to spend this month?” If your goal is $4,000 and you are on pace to spend $3,000, you know you’re in good shape. If you’re on pace to spend $5,000, you’ll know you need to have a turkey sandwich instead of sushi for dinner. Keep it simple and avoid surprises!

Indeed, this approach won’t solve all your planning needs. More complex tax calculations and the very long-term impact of investments or withdrawal strategies should be handled with more sophisticated software, like the technology we have access to at Legacy. However, having a base knowledge of what your spending looks like by using a cash flow forecast can lead to much more fruitful collaboration with your financial planner or tax professional when planning for the long term.

If spreadsheets aren’t your thing, just let us know! We’ll create a customized template you can use to get on track.