2021 3rd Quarter Review:

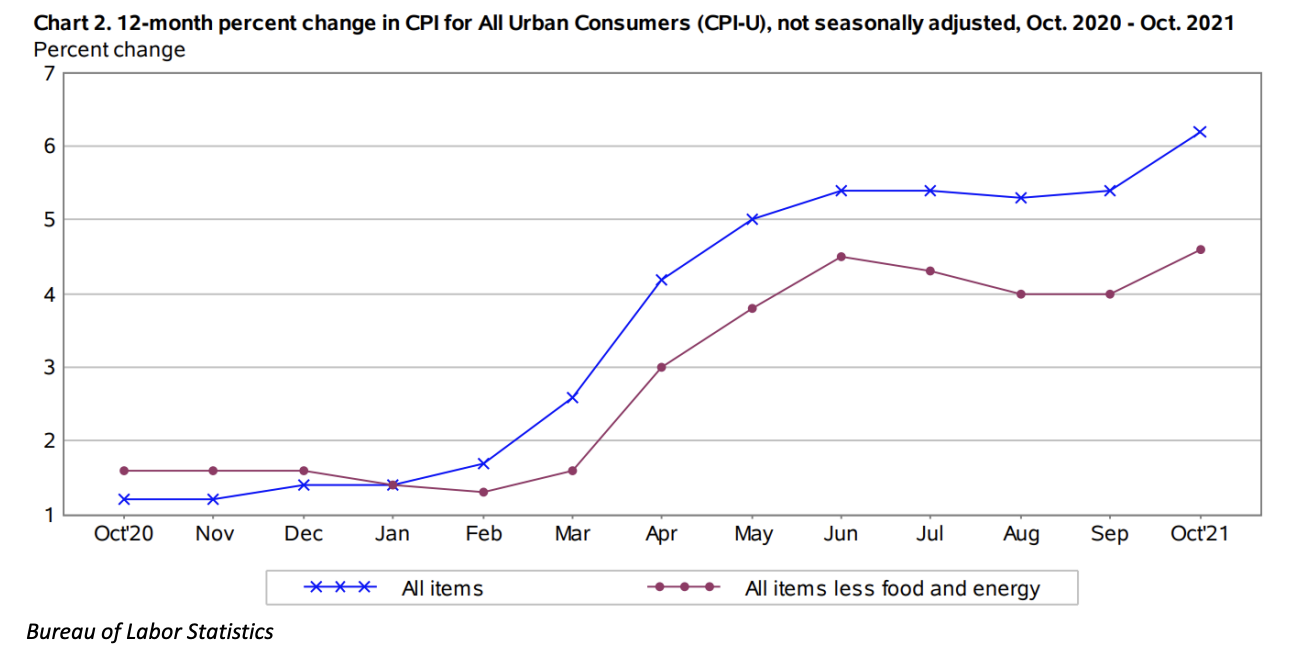

- October headline inflation is up +6.2% year-over-year (+4.5% excluding food & energy)

- Used vehicles and energy are still large outliers contributing roughly 3% of the total

- Several sub-categories contributing more meaningfully lately causing concern

- Supply chain disruptions and labor shortages contributing to price gains

- The cost of gasoline is less today than 2014 adjusted for inflation

Federal Reserve Chairman Jerome “Jay” Powell has maintained that inflation is transitory. With the exception of a brief bout of “inflation anxiety” back in February, the stock and bond markets have believed him. Today however, markets are declining in response to the highest inflation reading since October 1990. The concern is the breadth of price increases over the last 12 months in the Bureau of Labor Statistics (BLS) report: Energy +30%, Food at Home +5.4%, Food Away from Home +5.3%, New Vehicles +9.8%, Used Vehicles +26.4%. The “relative importance” of each varies but the numbers are larger than the 3% long-term average. Energy is the largest jump so let’s put it in perspective. An analysis conducted by Fund Strat Advisors determined that consumer expenditures on gasoline is less today than in 2014 (when we last saw oil prices this high) after adjusting for inflation and wages.

The chart above illustrates that the increase in CPI has coincided with vaccination distribution and economy re-opening when consumers began visiting stores and making purchases beyond the essentials like toilet paper and wine (Alcohol & Tobacco +8.5%). Supply chain disruptions and labor shortages affect everything from manufacturing to shipping and are the most noted and obvious explanations. The picture below provides a visual of the backlog. There is an estimated 100+ ships sitting idle in the Pacific ocean waiting to be unloaded. It’s a good thing Santa has a sleigh!

Inflation affects more than the grocery bill or gas pump receipt. Bond investments in particular are negatively affected. Most bond interest payments are fixed. If prices are going up, the future interest payments don’t compensate you enough for the cost of stuff. Investors lose “purchasing power” and bond prices fall as a result. Higher inflation leads to higher short term rates which leads to a decrease in the expected return of stocks. Some industries are more affected than others.

In summary…

Patience is not only a virtue but a requirement in investing. We are closely watching the data but not concerned at this time. It is very difficult to accurately predict when supply chain and labor issues will normalize. Therefore, it is equally difficult to know if higher inflation is transitory or could negatively impact portfolios. For now, our inflation outlook is 2.0% – 2.5% longer-term (higher than the past 10 years). Stocks have been the best hedge against inflation over time so we are maintaining exposure. Our view is that bond returns will be less than longer-term averages but necessary to manage risk. We are visiting with clients individually to determine if more stocks (or less) is appropriate.

As always, we genuinely appreciate the trust you place in your financial advisor and our firm.